CMS

TL;DR

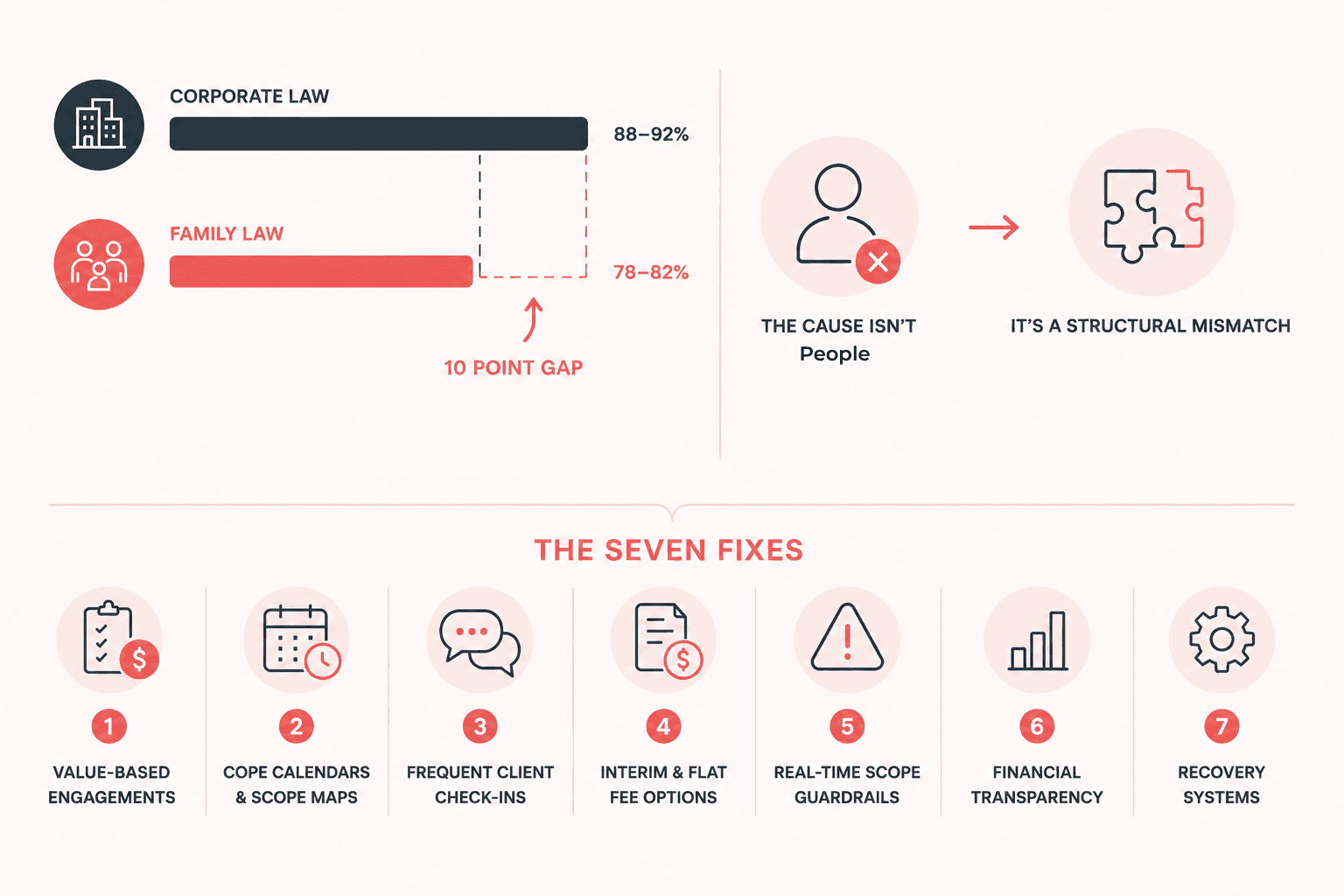

Family law firms collect 78–82% of what they bill, the lowest realization rate of any major legal practice area, roughly 10 points behind corporate law. The cause isn't bad lawyering or bad clients. It's a structural mismatch between how family law work gets done (emotional, unpredictable, high-conflict) and how legal billing was designed (rational, predictable, post-hoc). The seven fixes below address each failure point with named systems firms can adopt this quarter.

The numbers nobody talks about

Family law has a quiet collection problem that the rest of legal doesn't.

According to the most recent Thomson Reuters Legal Industry Report and Clio Legal Trends data, family law firms post realization rates between 78% and 82% which means for every dollar of work performed, 18 to 22 cents never makes it to the bank. Corporate law firms, by contrast, sit at 88–92%. Personal injury runs on contingency so the comparison isn't clean, but criminal defense, another emotionally charged consumer-pay practice, still beats family law by 4–6 points.

That gap isn't randomness. It's the predictable output of a specific set of structural problems.

Here's what makes family law uniquely bad at getting paid, and what to do about each cause.

Why family law collection rates are structurally worse

Most articles on legal AR blame "bad client communication" or "weak follow-up." That's a symptom, not a cause. The real drivers are five overlapping forces unique to family practice:

1. Emotional decision-making at intake. Clients hire in crisis. They overestimate their willingness to pay later because the pain of the matter is acute now. Six months in, when the divorce is grinding and the legal bill is real, the same client makes a very different calculation.

2. Adversarial trust collapse mid-matter. Unlike corporate litigation where the opposing party is a faceless company, family law clients are fighting people they used to love. As trust collapses with the ex-spouse, it often collapses with everyone billing them, including their own attorney. Bills get reframed as another form of victimization.

3. Liquidity transfer happens during the matter. Joint accounts get frozen. Houses get sold mid-case. The client who could afford you in month one cannot in month seven. Other practice areas don't have a billing window that overlaps with the client's primary source of liquidity literally being divided in court.

4. Form-heavy work creates "I could have done this myself" resentment. When a client gets a $4,800 bill and 60% of the line items are FL-100, FL-140, FL-142, FL-150 preparation, they don't see legal judgment, they see paperwork. Paperwork they suspect they could have filed for free. (For context on what these forms actually require, see Aparti's guide to the FL-100 form.)

5. The case ends before payment does. Divorce decrees get entered. The client moves on emotionally. The remaining balance becomes "the past." Other practice areas have ongoing relationships that incentivize settling up. Family law typically does not.

These aren't excuses. They're the diagnostic. Each of the seven fixes below maps to one or more of these structural causes.

The 7 fixes that work

Fix 1: The Intake-Stage Collection Triage

What it is: A structured 12-minute intake protocol that scores every prospective client on five collection-risk factors before the engagement letter is signed.

Most firms intake on legal viability. Strong firms intake on collection viability. The five factors:

Factor | Question | Risk signal |

|---|---|---|

Liquidity source | Where will fees come from? | Joint accounts soon to be frozen = high risk |

Conflict temperature | Is the other party retained? Litigating or negotiating? | High-conflict litigation = high risk |

Emotional regulation | How is the client describing the ex? | Extreme language = high risk |

Prior counsel | Has the client fired previous attorneys? | Two or more = very high risk |

Expectation gap | What does the client think this will cost? | Off by 3x or more = high risk |

Clients scoring high on three or more factors get either declined, scoped into limited-scope representation, or required to maintain a larger evergreen retainer. This single change moves a typical family law firm's collection rate by 3–5 percentage points within two billing cycles.

This isn't about avoiding hard cases. It's about pricing risk into the engagement structure before the work begins.

Fix 2: The Evergreen Retainer Floor

What it is: A non-negotiable minimum trust balance that triggers automatic replenishment requests before — not after — work is performed against it.

The old model: collect a $5,000 retainer, bill against it, ask for a refill when it hits zero.

The problem: by the time the trust account hits zero, the client is already in financial stress, already emotionally fatigued, and already starting to perceive bills as adversarial. The refill request becomes a fight.

The replacement: set a floor, typically 40% of the initial retainer, and trigger replenishment automatically when the balance drops below it. The client always sees a "healthy" trust balance. Replenishment becomes routine, not crisis.

Firms that adopt this see their average days-to-replenishment drop from 22 to under 7, and their write-off rate on uncollected post-retainer work drop by roughly half.

Managing this manually, tracking balances across every active matter, timing replenishment requests, following up when clients don't respond, is where most firms fall short. Aparti monitors trust balances in real time, triggers automated replenishment reminders at the right threshold, and handles follow-up sequences so the process runs without anyone on your team having to remember to check.

Fix 3: Form Automation as Margin Protection

What it is: Moving high-volume, low-judgment form preparation (FL-100, FL-140, FL-142, FL-150, UCCJEA, ATROs) off the billable timesheet and onto automation, then repricing the engagement around legal judgment.

This is the single most underrated lever in family law economics, and it's where the perception of "I could have done this myself" gets neutralized.

When form preparation is billed hourly, three things go wrong:

The client sees a bill dominated by clerical-feeling tasks

Associates and paralegals spend cognitive load on low-leverage work

The firm has no real margin on the work because the hourly rate has to be defensible against a paralegal benchmark

When form preparation is automated, the firm bills for what the client actually values, strategy, negotiation, court appearances, judgment calls, and the forms become a fixed-cost line item or a flat-fee inclusion.

Aparti's AI software for auto-generating California divorce forms is one approach to this. The deeper point is structural: any system that removes form prep from your hourly billing surface area will improve your collection rate, because the lines that get disputed most often are the ones that look like clerical work.

Fix 4: The Mid-Matter Financial Check-In (The 90-Day Reset)

What it is: A scheduled, non-billable 20-minute conversation at the 90-day mark of every matter to recalibrate expectations on cost, timeline, and scope.

The biggest predictor of a write-off is the gap between what the client expected the case to cost at intake and what it actually costs at the 6-month mark. Closing that gap requires deliberate conversation, not better invoices.

The 90-day reset has a fixed agenda:

Where the case actually stands versus the intake projection

What's driving any cost variance (typically: opposing counsel behavior, discovery, custody disputes)

What the next 90 days will likely require

Any changes to the client's liquidity or payment ability

This conversation is uncomfortable. Firms that hold it religiously report dramatically lower write-offs. Firms that skip it discover the client's financial reality only when invoices start aging past 60 days — at which point recovery is much harder. See Aparti's analysis of why family law firms struggle to get paid on time for the underlying dynamics.

Fix 5: The Litigation-Adjusted Fee Schedule

What it is: A two-tier fee structure that explicitly prices high-conflict, litigation-track matters differently from negotiation-track matters, communicated transparently at engagement.

Family law firms tend to use one hourly rate for everything. But the realized economics of a high-conflict trial-track case look nothing like a stipulated dissolution. Trial-track work has:

2–3x the unbillable communication overhead

Significantly higher write-off risk

More court-driven schedule volatility

More emotional load on attorneys (and therefore more attrition cost)

A two-tier schedule prices that reality in. Litigation-track engagements carry a 15–25% premium and require a larger evergreen retainer floor. Negotiation-track engagements get the standard rate. Clients who think they're negotiation-track but trigger litigation behaviors get repriced at a defined inflection point (typically: filing or responding to an OSC, designating experts, or any restraining order activity).

This protects the firm from the most common write-off scenario: a case that was scoped as a settlement and quietly became a war.

Fix 6: The Pay-Through Mechanism

What it is: A structured arrangement where a portion of the marital estate is set aside at the start of the matter, by stipulation, court order, or escrow, specifically to fund both parties' fees.

This is the most underused tool in California family law and similar jurisdictions. Family Code §2030 and §2032 explicitly contemplate fee orders to balance the parties' ability to litigate. But fee motions are typically filed reactively, when one party can no longer pay, rather than proactively as part of case management.

A pay-through mechanism, established early, can take the form of:

A stipulated set-aside from a pending real estate sale

A court-ordered advance from community funds

An escrow funded by liquidating a specific community asset

A pendente lite fee order under §2030

When fees are coming from a defined, court-blessed source rather than from a client's ongoing personal cash flow, collection rates approach corporate-law levels. The work is done; the funding source has been pre-approved; disputes become rare.

Fix 7: The Closeout Protocol

What it is: A structured, non-negotiable sequence run in the final 30 days of every matter to surface and resolve any remaining balance before the case concludes.

Most family law write-offs happen after the case closes. The decree enters, the client's emotional engagement drops to zero, and any balance becomes "the past." The window to collect closes faster than most firms realize.

The closeout protocol runs in the 30 days before judgment:

Day -30: Run a full statement reconciliation; flag any line items the client has questioned

Day -21: Schedule a closeout call; preview the final invoice

Day -14: Send the projected final invoice with a payment plan offer if the balance is meaningful

Day -7: Confirm payment method on file; arrange autopay for any post-judgment balance

Day 0: Judgment entered; final invoice sent same day; payment processed within 72 hours

The single most predictive variable for whether a balance gets collected is whether it gets resolved before the judgment is entered. After judgment, recovery rates drop by more than half. For deeper context on this dynamic, see Aparti's article on navigating the family law AR crisis.

How these fixes stack

The seven fixes aren't independent. They compound:

Fixes 1 and 2 (intake triage + evergreen floor) work upstream of the matter

Fixes 3 and 5 (form automation + tiered fees) reshape the engagement economics

Fixes 4 and 7 (90-day reset + closeout) protect against expectation drift

Fix 6 (pay-through) reroutes the funding source entirely

Firms that adopt three or more of these systems consistently push realization rates above 90%, closing the gap with corporate law entirely. Firms that adopt all seven tend to outperform corporate law on this metric, because their per-matter administrative overhead is lower and their collection cadence is faster.

What this means for the firm of the next five years

Family law's collection problem is solvable, but not by working harder at the existing model. Every fix above has the same shape: it moves the firm from reactive billing to structured billing, and from undifferentiated services to explicitly priced ones.

The firms that survive the next AR cycle won't be the ones that work harder on collections. They'll be the ones that have moved form preparation off the timesheet, structured their retainers to refill automatically, and built closeout protocols that finish the matter financially before it finishes legally.

The technology to do this, AI-assisted form automation, automated trust account monitoring, structured intake scoring, exists today. The methodology questions are now the binding constraint.

For a closer look at how AI is reshaping family law specifically, see Aparti's overview of the best AI software for family law firms and the broader piece on how AI is changing the divorce process.

Frequently asked questions

Why is the family law collection rate worse than other practice areas? Family law combines emotional clients, mid-matter liquidity disruption, and a high proportion of form-based work that clients perceive as clerical. These three factors together produce realization rates 6–12 points below corporate law and 4–6 points below criminal defense.

What is a good collection rate for a family law firm? Industry median is 78–82%. Top-quartile family law firms hit 88–92%. The realistic ceiling, with all seven fixes in place, is 92–95%.

How do I move form preparation off my hourly timesheet without losing revenue? Reprice the engagement so legal judgment carries the rate, and bundle automated form preparation as a flat-fee inclusion. Most clients perceive this as more transparent, not less valuable, and the firm captures higher margin per attorney hour.

Is an evergreen retainer legal in California? Yes, when properly structured. The retainer must be held in trust under Rule 1.15, and replenishment terms must be disclosed in the engagement agreement. Most state bars permit evergreen structures with appropriate trust accounting.

When should I file a §2030 fee motion? The strongest practice is to evaluate §2030 viability at intake, not in crisis. If there's a community asset that could fund both parties' fees, a stipulated set-aside or early fee order produces dramatically better collection economics than a reactive motion filed when a client stops paying.

What's the single highest-leverage fix? If a firm can only adopt one, automated form preparation (Fix 3) produces the largest economic impact because it changes both what the firm bills for and what clients perceive as billable. The intake triage (Fix 1) is the highest-leverage upstream fix.

Related reading

AI Software to Auto-Generate FL-100, FL-140, FL-142, FL-150 California Divorce Forms

Understanding the FL-100 Form: Your First Step in California Divorce

How AI Is Revolutionizing the Divorce Process

Aparti offers a billing intelligence software built for family law firms, purpose-designed to close the gap between what you bill and what you collect. From automated AR follow-up and trust account monitoring to collection-risk dashboards and matter-level payment tracking, Aparti gives your firm the financial visibility to stop leaving 18–22 cents of every billed dollar on the table.

" height="16.57165px" id="usoExa717" transform="translate(1 2)" width="18.33337px"/></svg>)

" height="19.996073000000003px" id="slKA4m0c7" transform="translate(0 0)" width="19.9883px"/><path d="M 5.137 0 C 2.301 0 0 2.301 0 5.137 C 0 7.973 2.301 10.273 5.137 10.273 C 7.973 10.273 10.273 7.973 10.273 5.137 C 10.273 2.301 7.973 0 5.137 0 Z M 5.137 8.469 C 3.297 8.469 1.805 6.977 1.805 5.137 C 1.805 3.297 3.297 1.805 5.137 1.805 C 6.977 1.805 8.469 3.297 8.469 5.137 C 8.469 6.977 6.977 8.469 5.137 8.469 Z" fill="rgb(232, 124, 124)" height="10.273390000000001px" id="QoooNkCCR" transform="translate(4.863 4.863)" width="10.27342px"/><path d="M 2.399 1.199 C 2.399 1.863 1.859 2.398 1.199 2.398 C 0.535 2.398 0 1.859 0 1.199 C 0 0.535 0.539 0 1.199 0 C 1.859 0 2.399 0.539 2.399 1.199 Z" fill="rgb(232, 124, 124)" height="2.3984400000000003px" id="QF02FX4CF" transform="translate(14.141 3.461)" width="2.398500000000002px"/></g></svg>)

" height="19.999972999999997px" id="cGbUHvSUM" transform="translate(0 0)" width="20px"/></g></svg>)